We believe that the most consistent source of return comes from understanding valuations and allocating our assets to areas of value. It is from valuation too that the best understanding of risk comes. Therefore at the heart of our process is a methodology that allows us to understand the risk / reward trade-offs of very different asset classes in a comparable manner.

Asset allocation is widely accepted as the most important step in portfolio construction. Our dynamic asset allocation process focuses both on which assets to own and the right combination of the assets so the overall portfolio behaves positively across a wide range of economic scenarios. Equity markets can be very volatile - diversifying the portfolio by including various asset classes can lower the overall portfolio risk. We utilise a broad range of asset classes and strategies. By increasing the opportunity set of available asset classes we are able to increase the level of true diversification in the portfolio. We combine assets that vary in response to market-driving forces, leading to more consistent returns.

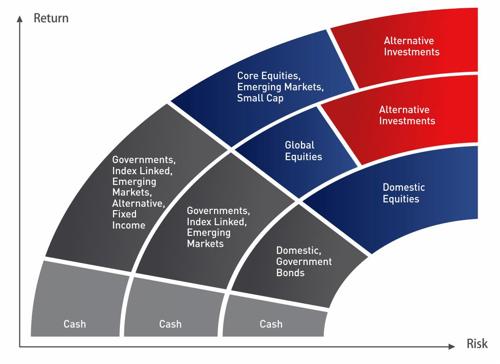

Asset class selection is our starting point

Our first focus is to determine the relative attractiveness of asset classes based on our assessment of the macroeconomic environment, valuations and investor sentiment. Our starting point is an assessment of valuation. We look at asset classes in an absolute sense relative to their own history and also relative to other asset classes.

We model and scenario test likely returns for each asset class. We compare valuation versus our bottom-up five year expected returns and on top of this we overlay different economic scenarios to stress test the prospective returns.

We have found that this process often throws up anomalies in terms of entire asset classes being mispriced, either for the better or the worse. These mis-pricings are the starting point for our asset selection and portfolio construction.

Our ideal is to find asset classes that are likely to meet our long term return criteria irrespective of the path of the wider economy.

By tilting a portfolio’s exposure between different asset classes at different times there is value to be earned, in the form of enhanced returns and/or reduced risk, which is the premise behind tactical asset allocation. This active method of portfolio management aims to add to or take from different asset classes within the portfolio depending on valuations and the outlook for a particular asset class at that point in time.

Many investors simply allocate among the asset classes popular at the time in proportions similar to those of other investors. While this usually creates uncontroversial portfolios, it often leads to substantial weightings in whatever the asset class of choice is at a particular point in time. Our approach avoids making allocations based on the fashion of the day.

Our active asset allocation decisions always begin with our five year expected returns framework. We dedicate significant resources to maintaining a wide range of long term expected returns across numerous regions and asset classes, each of which is updated monthly. Our aim is to focus portfolios towards asset classes that are undervalued relative to their long term return potential, where there is a ‘margin of safety’ that reduces the probability of losses. This framework is designed to distinguish, in a consistent and unemotional manner, between a good investment story – such as a strong economic backdrop in the US – and a bad investment opportunity – when all the good news is already discounted in prices and downside risk may be elevated. Macro and micro-economic conditions are constantly monitored, discussed and debated, but the foundation of any asset allocation decision we make is always the valuation. The investment team will adjust asset allocation as return expectations evolve and opportunities arise.