Alex Harvey - Senior Portfolio Manager & Investment Strategist

Alex Harvey - Senior Portfolio Manager & Investment Strategist

The new year brought little in the way of new order as on 3rd January President Trump launched US strikes in Venezuela that culminated in the capture of Nicolás Maduro and the abrupt disruption of the Bolivarian leadership. At the time this was huge news, albeit not very impactful on financial markets, but it set a strong tone for and clear intent for how the US administration looked set to move forward. Whilst the oil price flickered, and despite the country having the largest proven oil reserves, its estimated 1% of global production it did little to move prices in any meaningful way. More impactful has been the increased tension and build-up of US military hardware around the Persian Gulf. The world was horrified to see images of what is rumoured to be the bodies of thousands of Iranians killed as part of the mass protests across the country against the regime. Protester deaths were not confined to Iran, and the US administration found itself increasingly under pressure following the deaths of two protesters in Minneapolis at the hands of Trump’s ICE patrols. Under the premise of securing a nuclear deal, and perhaps to deflect from these domestic problems, the US is amassing a ‘huge armada’ in scenes reminiscent of Venezuela just weeks ago, the difference here being that the action taken against the South American country falls under the so called ‘Monroe Doctrine’, whereby the US asserts a growing sphere of influence over its western hemisphere neighbours. This culminated in an increasingly hostile dialogue with Denmark over ownership of the autonomous territory of Greenland, a prize Donald Trump was seeking for Arctic security reasons. The situation defused on the military dimension (but not diplomatically) after the President spoke at Davos, appearing to rule out military action.

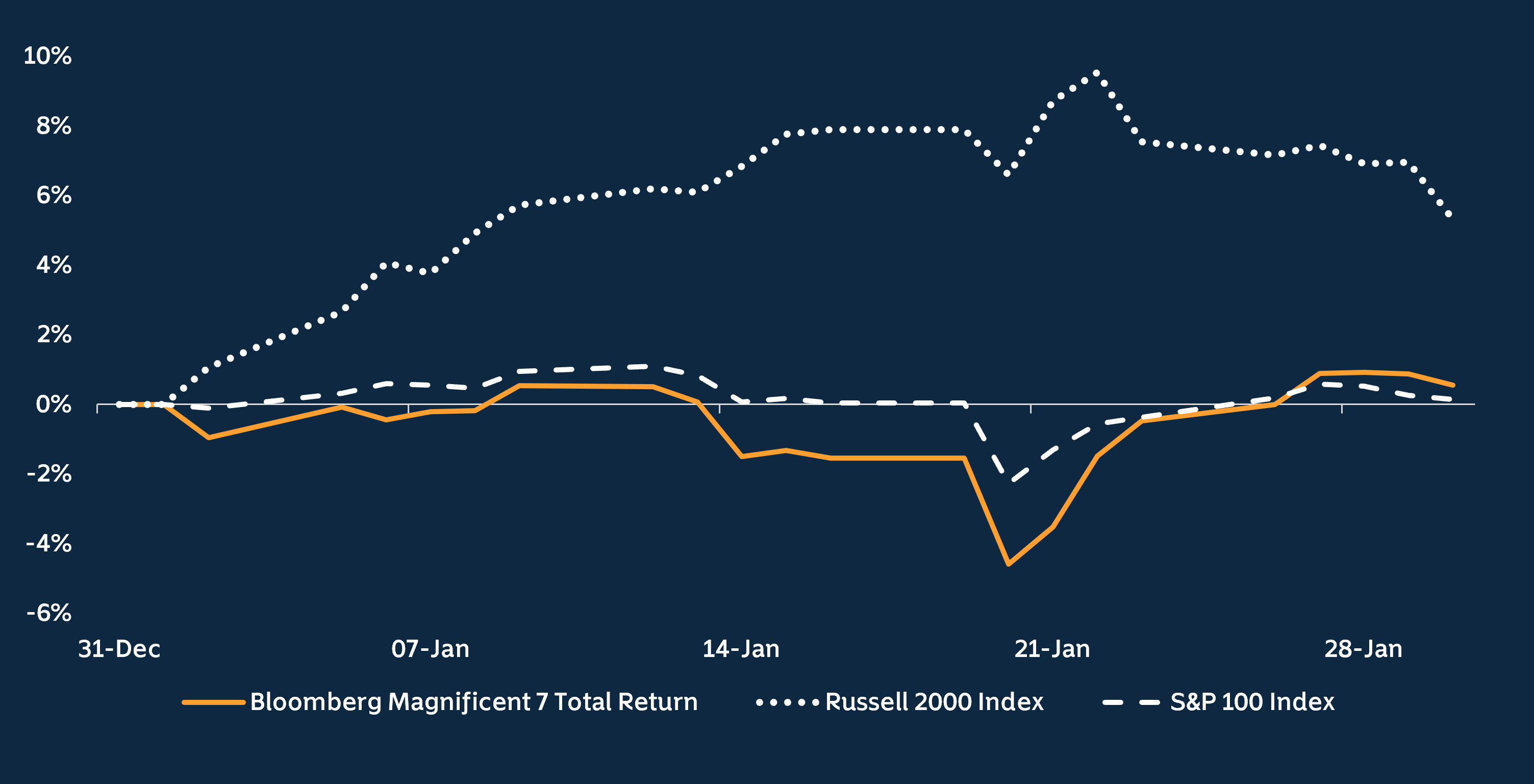

All the above would provide ample material for a quarterly or even annual commentary but remarkably this has played out in just a couple of weeks. Were this kind of geo(ego?)-political posturing something new for financial markets to digest, one might expect risk assets to perform less well, and treasuries to make gains. Conversely however, investors have become accustomed to what are arguably market moving events playing out in this way, and absent a model to price this ‘Trump risk’, markets have again chosen to look through the near-term noise. One upside perhaps of the marginalisation of these events, is a focus on corporate and economic fundamentals, which ultimately will drive asset class returns over the longer term. In the US, which accounts for over 70% of the MSCI World Index, fourth quarter earnings season started well, with strong positive sales and earnings growth coupled with upside surprise. The economy remains in reasonably good health, and inflation somewhat in check, such that the Fed held rates at their January meeting. What was encouraging to see was a broadening out of the equity rally with small caps outperforming mega cap by some margin (6%). The Russell 2000 index of US small cap stocks added 5% versus the Magnificent Seven’s -0.3%. Whilst Japanese shares fared less well, no doubt hampered by a strong Yen as rumours of intervention surfaced, broader Asian equities did well, led by the still supercharged Korean market which added 24% in January, on top of 2025’s near 80% gains. Emerging market equities more broadly rallied on the back of buoyant risk appetite – despite the aforementioned geopolitical events – and the continued headwind facing the US dollar, down 1.4% on the month, and continuing a trend which saw 11% come off the DXY index in 2025. Bonds on the whole posted positive but unexciting returns during the month, notwithstanding some tumultuous price action at the long end of the Japanese bond market.

Equity markets broaden out - Large Caps vs. Small Caps

Source: Bloomberg Finance L.P., as at 30 January 2026

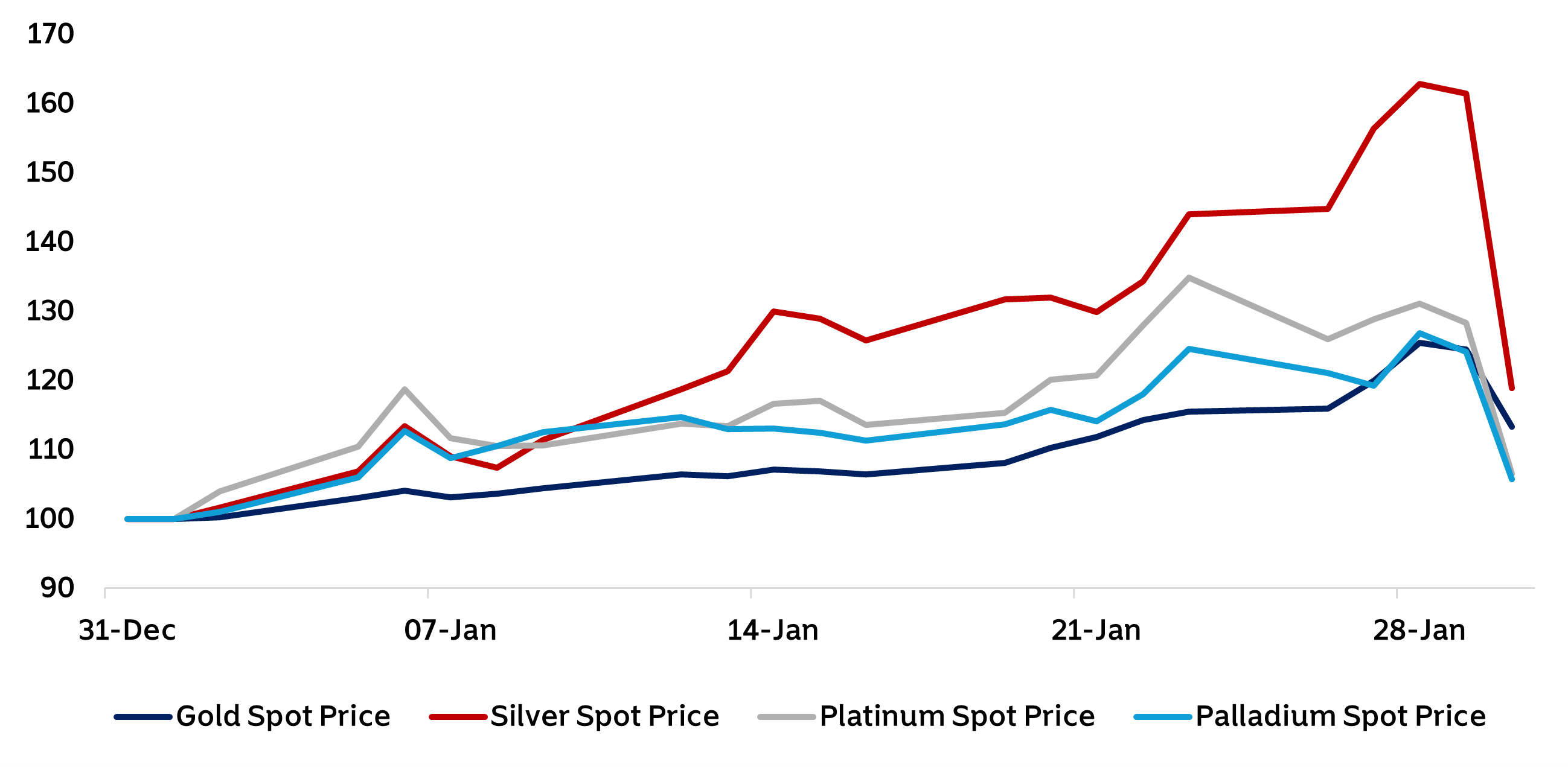

The ’debasement’ trade, as it’s being termed, continues to dominate the narrative and to fuel a spectacular rally in gold and precious metals more broadly (despite a crash in late January). Having gained over 25% during the month the yellow metal fell back to add 13% during the month, and silver ‘only’ 19%. Whilst the thesis of debasement perhaps holds intact over a longer-term horizon, and an element of idiosyncratic US country risk plays its part, these kinds of returns don’t really square with a 1.4% fall in the dollar index. Although commodities are by their nature hard to value, with prices determined squarely by supply and demand and cyclical factors, it feels hard not to think that precious metal prices are still somewhat extended at this time. What this does tell us, even if you strip out the momentum buying, is that investors remain concerned about wider risk that pervades markets and which our own proprietary risk measures show as somewhat underpriced – the corollary being that markets are exhibiting a degree of complacency. Whilst we continue to favour owning risk assets, we stress the importance of remaining diversified and are happy to own quality at what is arguably a discount in markets today. Cream always rises to the top.

Precious metals pull back after big monthly gains

Source: Bloomberg Finance L.P., as at 30 January 2026.