Alex Harvey, CFA - Senior Portfolio Manager & Investment Strategist

Alex Harvey, CFA - Senior Portfolio Manager & Investment Strategist

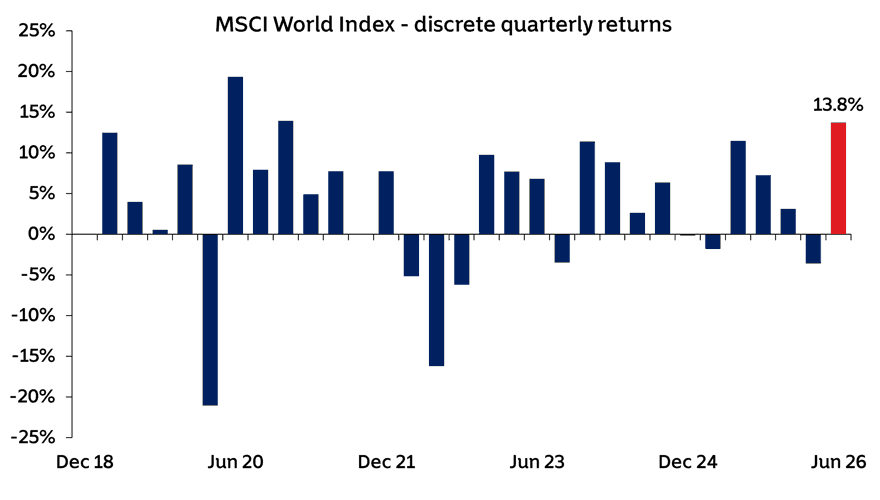

The 10% year to date return from global equities masks the best quarterly performance since Q4 2020 when ‘Vaccine Monday’ provided a financial adrenaline shot to markets. Indeed, the 13.8% return would be welcome in any calendar year, let alone over a three-month period. Clearly, the about-turn exercised by risk assets since 30th March, following (yet another) ceasefire announcement, flatters the discrete quarterly performance; on a rolling basis markets rallied harder post the tariff tantrum nadir in April 2025. Nonetheless, this is welcome performance against a challenging backdrop and a persisting war rhetoric. Yes, a Memorandum of Understanding (MoU) was signed between the US and Iran (some say ‘Misunderstanding’ is more appropriate), but as we’re witnessing at the time of writing it is far from lasting, peace remains fragile and maritime traffic at risk.

Source: Bloomberg Finance L.P., as at 30 June 2026.

Aside the continuing US war with Iran, which concurrently saw an escalation of Israel’s bombing in Lebanon over the period as Prime Minister Benjamin Netanyahu looked to expunge Hezbollah militants, we also had a Trump-Xi meeting in Beijing, a new Chairman of the Federal Reserve (Fed) appointed and even a UFC (Ultimate Fighting Championship) event on the White House lawn to celebrate 250 years of the United States and Donald Trump’s 80th birthday. Classy. Closer to (MGIM’s) home the UK Prime Minister came under renewed pressure as Andy Burnham, the former Mayor of Manchester, won the Makerfield by-election putting him on course to challenge for the leadership, resulting in Sir Kier Starmer announcing his resignation to make way for a new Labour party leader and UK Prime Minister who will be the seventh in the last ten years. The world was spared another pandemic but the news in early May that passengers aboard a cruise ship were falling ill with hantavirus was eerily reminiscent of the early days of Covid. This outbreak was swiftly contained but sadly the Ebola outbreak in West Africa continues to spread, the effectiveness of the response arguably constrained by reductions in US funding to African aid organisations. Thousands have been infected across the Democratic Republic of Congo (DRC) with hundreds dead including 32 healthcare workers.

With the backdrop of continuing wars, rampant government bond issuance and a resilient consumer, the inflation risk still appears more to the upside than towards central bank targets. President Trump appointed Kevin Warsh as the new Chairman of the Fed with the express desire to see rates engineered lower, but US policy rates remained unchanged over the quarter as a slew of data made it all but impossible for the Board of Governors to cut rates at this time, extending the pain borne by consumers in recent years as policymakers have battled to tame price rises after the twin supply and demand shocks presented post covid, resulting from a strong consumer with a propensity to spend, rising energy prices and supply chokepoints. A couple of bumper non-farm payroll reports for April and May only added to the higher rate narrative, but a softer June reading and a revision lower for May, released after the quarter end, has bought Mr Warsh some wiggle room to paint a more balanced outlook for policy going forward. The market though is still pricing an effective Fed policy rate of 4% at year end, amounting to an implied 1.5 rate hikes of 25bps each at the time of writing. The Bank of England (BoE) also found its hands tied with inflation printing above target, making it difficult to provide some much needed relief to the lacklustre economy, which is barely generating any growth in real terms, despite a modest revision higher for the first quarter of the year. Of the other major central banks, both the ECB and the Bank of Japan in June raised their respective policy rates by 25bps each to thwart any inflationary pulse. It is no coincidence that both regions are heavy importers of energy and against the geopolitical backdrop they are arguably more exposed than other major developed economies, certainly more so than the US which today is the leading global producer of oil and natural gas and more insulated from the energy shock of the Iran and Ukraine wars.

It was an overwhelmingly strong period for investment returns over the quarter, with risk assets posting double digit gains in most markets and regions. Growth and technology stocks roared back to life, after the uncertainty that plagued the first quarter appeared to disappear (temporarily at least). The Philadelphia Semiconductor Index posted a whopping 88% return over the three-month period as rampant demand for all things ‘chip’ fuelled the next wave of the AI capex rollout. The trailing price to earnings ratio of that index topped 80x before falling back. With the forward multiple hitting 35x, the implied earnings growth of almost 130% over the next 12 months is almost unprecedented. There is little room for disappointment. In a similar vein and supporting the positive sentiment around the technology sector was the much-hyped and highly anticipated initial public offering (IPO) of SpaceX, Elon Musk’s rockets-to-data centre venture that ‘popped’ almost 70% higher from its launch pad price on its second day of trading, which also proved to be its apogee as it has since traded back to just a 7% premium to its $135 debut. IPO fervour is certainly in the air with OpenAI and Anthropic lining up their own public offerings. The race for capital isn’t confined to the upstarts however, nor just equity, as the hyperscalers ramp up debt issuance which analysts forecast could top $200bn this year, not far off double last year’s $120bn. Alphabet – the parent company of all things Google – also stole a march on these young pretenders by raising $84bn in its first large scale equity raise since 2010 and its largest for 22 years. Whilst this backdrop appears bullish, one has to wonder why the likes of Alphabet and the AI companies are clamouring to sell their equity, especially when the debt markets are very much open for business.

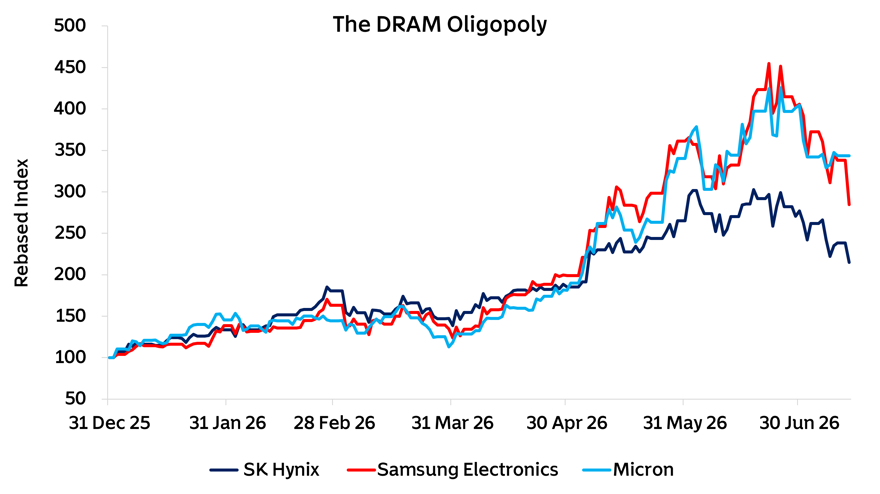

Source: Bloomberg Finance L.P., as at 30 June 2026. * DRAM is Dynamic Random-Access Memory.

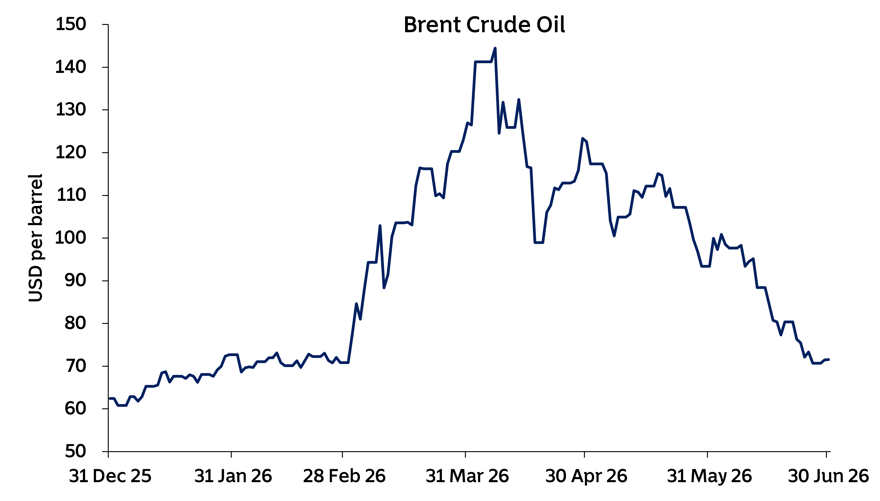

Non-US regional equities on the whole did very well. Emerging markets and Asia ex Japan gaining 23% and 27% respectively, dragged higher by the still surging but concentrated Korean and Taiwanese markets (68% and 45%) comprising the likes of SK Hynix, Samsung and TSMC. Indeed, if you thought the US was concentrated spare a thought for these markets where TSMC represents 30% of the benchmark index and SK Hynix and Samsung together 50% of the KOSPI. The laggard performer was China and whilst the domestic A shares market mustered some gains, the MSCI China and Nasdaq Golden Dragon indexes both ended the period in the red. Bonds mostly clipped coupons over the quarter with the carry from higher starting yields offsetting some modest price pressure to offer up some positive total returns. Public US high yield bonds and loans made low single digit returns but stayed comfortably unruffled by the long queue of investors wanting to redeem from private credit funds in the US. Commodities were led lower for the most part, certainly at the aggregate index level, by falling oil and gas prices. Spot Brent crude prices were down some 40% from the end of March, largely coinciding with the efforts to open up the Strait of Hormuz through ending the war and ‘Project Freedom’, the US President’s initiative to ensure safe passage for commercial vessels. Gold was also a casualty, bucking its recent trend of acting more like a risk asset than a defensive one, and almost reasserting its long held inverse relationship with real rates. Unsurprisingly, silver followed the yellow metal lower, just by more, and Bitcoin – ‘digital gold’ to some – fell over 13% during the period; half its 27% pullback year to date, and more than 50% down from its October peak.

Source: Bloomberg Finance L.P., as at 30 June 2026.

As we go into the second half of the year not a lot on the surface has changed. War remains a staple of newsflow, inflation remains sticky, consumers somewhat resilient and markets buoyant. What does seem clear is that volatility is likely to remain elevated as liquidity and demand for innovative financial products (think leveraged single stock ETFs) create whipsawing effects in highly cyclical markets, and a pipeline of IPOs that require funding could see a rotation of money from the old to the new. It is encouraging to see equity markets moving higher on earnings rather than multiples (valuation), as it is earnings that underpin returns over time, but investors should be mindful that the 25%+ earnings growth currently discounted by the US stock market for the next twelve months is a high hurdle to beat. Historically, the market’s expectations for future earnings have materialized, but in the absence of a valuation uplift it is the growth rate in earnings that is important for market returns, and this level of growth is rarely sustained for long. When coupled with the concentration risks discussed in this and previous communications, and the fragile geopolitical backdrop, staying invested but diversified by asset class, style and manager should be a top priority for investors today.